J.M. Keynes’ policy proposals were much more radical than you were probably taught in university6/29/2018

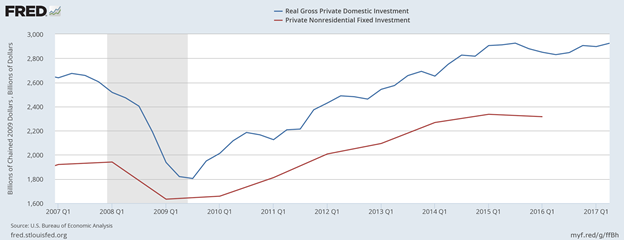

Contrary to what some economics textbooks might have you believe, John Maynard Keynes resoundingly rejected the classical paradigm, and, based on his policy prescriptions in The General Theory, he would have rejected the current mainstream macroeconomic policy tools of fiscal policy, taxation, and interest policy as the sole means of managing the business cycle. Rather, Keynes advocated for a much more interventionist role of government in public investment, “a somewhat comprehensive socialization of investment” as he referred to it, and a more long-term regime of low interest rate policy sufficient to push the economy to full employment. Keynes’ prognosis of the 1930’s economic malaise was due to the lack of effective aggregate demand which required sufficient investment to remedy. While public deficit spending could alleviate a downturn in the short-run, it would not be sufficient to prevent cyclical fluctuations in the long-run and keep the economy running at full-employment. As such, Keynes’ proposals could be considered quite radical relative to his time, and even current interventions used today. The current macro policy management kit consists of deficit spending and taxation (fiscal policy), and interest rates (monetary policy). Perhaps the best proxy for the mainstream (institutional) view on how these policy tools should be used is the current Federal Reserve Chair, Janet Yellen. Back in November, 2016, Yellen offered advice on fiscal policy just after the presidential election victory of Donald Trump. A major plank of Trump’s policy platform was infrastructure spending, but Yellen cautioned during congressional testimony to the Joint Economic Committee that “the economy is operating relatively close to full employment at this point,” so deficit spending would not have the same effect as it might have immediately after the Great Recession began in late 2007. She further cautioned that the new administration and Congress should be mindful of the debt: “With the debt-to-GDP ratio at around 77%, there’s not a lot of fiscal space should a shock to the economy occur, an adverse shock that did require fiscal stimulus.” Essentially, Yellen is suggesting that rather than wasting such an expenditure now, it would be better to save it until the next recession. On September 20th, 2017 Yellen gave remarks to the media regarding the Federal Open Market Committee’s decision to raise the federal funds rate from 1 percent to 1.25 percent, with a goal of 2.9 percent by 2020, as well as the announcement that the Fed will begin its “balance sheet normalization program” to reduce its nearly $4.5 trillion in securities holdings which resulted from its “quantitative easing” programs to reduce long-term interest rates. These decisions are indicative of the classical assumptions which have been embedded in New Keynesian macro theory, namely that the economy generally tends toward equilibrium, and these simple tools are sufficient for counter-cyclical management. As Yellen has testified, the mainstream establishment has the perception that the economy is doing better, and counter-cyclical tools are no longer necessary at this point. But, based on the proposals articulated in the The General Theory, Keynes would have disagreed. At the beginning of chapter 24 of his magnum opus, The General Theory of Employment Interest and Money, Keynes remarked that the two greatest flaws of modern capitalism were “its failure to provide full employment and its arbitrary and inequitable distribution of wealth and income.” The latter is made worse by the former, but both are viewed as non-issues in the classical paradigm. Progressive taxation has been one method by which to reduce inequality, but many worry about taking it too far; that it would reduce private investment and make the problem of unemployment and inequality that much worse. However, Keynes correctly identified that mass unemployment was caused by deficient aggregate demand, which in part was due to deficient investment. To address the issue of deficient investment, Keynes made two important proposals: 1) Low long-term interest rates equal to the marginal efficiency of capital. 2) The “socialization of investment.” The Fed’s quantitative easing (QE) program, which started under Chair Ben Bernanke, has been viewed as both innovative and extraordinary resulting in the long-term low interest rates since 2009. The purpose of this undertaking at the time was to provide a credible expectation to firms and entrepreneurs that rates of borrowing would be low for new capital investment. Despite QE, the shock of the downturn took a while to get over before private nonresidential investment began to pick up again in 2010 (see Fig. 1).  While one might be inclined to think that such a policy was original to Bernanke, in fact, Keynes advocated for central bank management of long-term interest rates through purchases of long-term securities in The General Theory (1936): [A] complex offer by the central bank to buy and sell at stated prices gilt-edged bonds of all maturities, in place of the single bank rate for short-term bills, is the most important practical improvement which can be made in the technique of monetary management…[However] The monetary authority often tends in practice concentrate upon short-term debts and to leave the price of long-term debts to be influenced by belated and imperfect reactions from the price of short-term debts; — though here again there is no reason why they need do so. The central bank can lower the short-term interest rates via purchases of short-term term securities in open-market operations, but this has no impact on long-term rates. Entrepreneurs and firms generally make long-term planning decisions based on what the government will do to short-term rates and may choose to hold off investment if they have reason to believe rates will not be favorable to them in the future. The central bank can address this by buying and selling long-term securities to provide a credible expectation that rates will be low in the long-term. This is indeed what the Fed did under Bernanke. But Keynes’ proposal was not that long-term rates should be kept low until the downturn was safely over and then raise them again. Instead, Keynes proposed low interest rates not only for the bust but also during the boom; even when the economy appeared to be “overheating” with wasteful investment and spending. [E]ven if over-investment in this sense [of being wasteful] was a normal characteristic of the boom, the remedy would not lie in clapping on a high rate of interest which would probably deter some useful investments and might further diminish the propensity to consume, but in taking drastic steps, by redistributing incomes or otherwise, to stimulate the propensity to consume… Thus the remedy for the boom is not a higher rate of interest but a lower rate of interest. For that may enable the so-called boom to last. The right remedy for the trade cycle [business cycle] is not to be found in abolishing booms and thus keeping us permanently in a semi-slump; but in abolishing slumps and thus keeping us permanently in a quasi-boom. The act of the monetary authority increasing interest rates has not only the effect of reducing investment, but also increasing unemployment, which in turn generates a further decrease in economic activity due to a decrease in demand. Thus, the current actions of the Fed to raise interest rates in a relatively meek growth environment, stagnant wages, and low labor force participation (relative to the pre-recession period) is exactly the opposite policy Keynes would have advocated. The level of aggregate demand depends on the level of employment and the propensity to consume, which is determined by the level of capital investment to create and expand firms to employ more people. However, due to the scarce nature of capital, sufficient investment alludes us and provides opportunity to the capitalist class to exploit that scarcity. “The owner of capital can obtain interest because capital is scarce, just as the owner of land can obtain rent because land is scarce. But whilst there may be intrinsic reasons for the scarcity of land, there are no intrinsic reasons for the scarcity of capital.” A means of reducing this scarcity, according to Keynes, is to “reduce the rate of interest to the level of the marginal efficiency of capital [net rate of return that is expected from the purchase of additional capital] at which there is full employment.” A low long-term interest environment can diminish the capacity to valorize capital in non-productive assets, pushing more investment into enterprise. [I]t would not be difficult to increase the stock of capital up to a point where its marginal efficiency had fallen to a very low figure. This would not mean that the use of capital instrument would cost almost nothing, but only that the return from them would have to cover little more than their exhaustion by wastage and obsolescence together with some margin to cover risk and the exercise of skill and judgement…Now, though this state of affairs would be quite compatible with some measure of individualism, yet it would mean the euthanasia of the rentier, and, consequently, the euthanasia of the cumulative oppressive power of the capitalist to exploit the scarcity-value of capital” (emphasis added). The “euthanasia of the rentier” would essentially be the castration of capitalist power over investment, and, therefore, over workers. However, interest rates alone are unlikely to be enough to ensure consistent investment up to the level of constant full employment, which brings us to Keynes’ other proposal. Looking at how “Keynesian” economics is practiced today, one would be inclined to think Keynes’ only contribution was to use government deficit spending on infrastructure, and, indeed, the U.S. infrastructure is in dire need of maintenance and would go a long way towards pushing the economy to full employment. However, Keynes wanted a more comprehensive intervention of the state in enterprise investment. “I conceive, therefore, that a somewhat comprehensive socialisation of investment will prove the only means of securing an approximation to full employment; though this need not exclude all manner of compromises and of devices by which public authority will co-operate with private initiative.” Keynes held these views for a long time. Prior to the publication of The General Theory, Keynes was active politically with the Liberal Party in Britain. According to James Crotty, in his book Capitalism, Macroeconomics and Reality: Understanding Globalization, Financialization, Competition and Crisis, Keynes was probably the “major force” in producing Britain’s Industrial Future (1928), a collective work of progressive proposals to improve Britain’s economy. Keynes proposed a new politically autonomous institution, like the Fed, called the Board of National Investment. Under the coordination of this “new and powerful” institution the state will be able to regulate the aggregate rate of growth of the economy by controlling the pace of public capital accumulation and directing investment toward the industries and areas hardest hit by structural unemployment. The Board was to control all the financial capital made available to public and semi-public concerns. It could borrow on its own account and was even authorized to lend to private companies. Keynes estimates that it would control 4 percent of GDP a year to start, and up to 8 percent of GDP in the foreseeable future.” This did not mean Keynes wanted a complete takeover of the economy by the state which he was careful to qualify in The General Theory: But beyond this no obvious case is made out for a system of State Socialism which would embrace most of the economic life of the community…[However] If the state is able to determine the aggregate amount of resources devoted to augmenting the instruments and the basic rate of reward to those who own them, it will have accomplished all that is necessary. Keynes clearly saw advantages in maintaining individual capitalism, mainly efficiency and personal freedom, and thought a comprehensive takeover of the state would sacrifice both as appeared to be the case in the Soviet Union in his time. But Keynes recognized that capitalism wasn’t perfect, it needed the strong guiding influence of the state to maintain full employment and temper the tempestuousness nature of the human economic activity which manifested so often in crises (e.g. The Financial Crisis).

If we define Keynesianism as the assumptions and tools used by macroeconomists today, then one may easily make the case even Keynes wasn’t a Keynesian. Keynes rejected erroneous assumptions about agents in the economy such as perfect competition, rational expectations, perfect foresight, and self-equilibrating markets. Simple manipulations of the interest rate and deficit spending have proven not enough to manage the economy and prevent crises. Keynes thought bigger and bolder with a larger role in mind for government to compensate for the inadequacies of capitalism; mainly as proposed in The General Theory, state control of investment and low long-term interest rates. The Fed was heading in the right direction by keeping interest rates low, but now it is regressing back again toward the status quo prior to the recession, raising interest rates at a time when wages are still stagnant and growth still relatively anemic. |

AUTHORAaron Medlin is a PhD student at the University of Massachusetts Amherst studying macroeconomics of private debt, monetary economics, international finance, and comparative economic systems. Archives

July 2020

Categories

All

|

- CV

- Dissertation

- Job Market Paper

- Research

-

Teaching

- Intro Micro - mock syllabus

- Intermediate Macro - mock syllabus

- International Finance - mock syllabus

- Comparative Econ Systems - mock syllabus

- Applied Time Series - mock syllabus

- Econometrics - mock syllabus

- Econ 191 Economics Behind Our Lives (Fall 2021)

- Econ 204 Intermediate Macro (Summer 2021)

- Econ 397: Debt Economics (Spring 2021)

- Commentary

RSS Feed

RSS Feed