|

There are many underlying factors which contributed to both the financial crisis and the Great Recession. The trigger of crisis and recession begins with the burst of the housing bubble in mid-2007. As subprime mortgage default rates began to accelerate, overly leveraged financial institutions holding risky products such as mortgage backed securities (MBSs) and collateralized debt obligations (CDOs) triggered a crisis of asset devaluation. Financial institutions holding both MBSs and CDOs and financial derivative products such as default swaps took a double hit inducing a liquidity crisis and immediate default risk. According to Crotty (2008), there are two major underlying causes which led to the financial crisis. The underlying causes are as follows: The first was bad theories such as the efficient financial market theory, and, generally, New Classical Macroeconomics. Such theories made assumptions at odds with the real world. For example, efficient market theory included assumptions such as: a) investors can determine the true distribution of risk; b) liquidity is never a problem; c) markets maintain stable equilibrium; d) default is rare; e) agent borrowing is limitless at risk-free interest rates. All of these assumptions turned out to be false. The second underlying cause was the “New Financial Architecture” which primarily consisted of flawed institutions and erroneous practices related to aggressive risk taking, over leveraging, and light government regulation. These practices inevitably led to stimulated aggressive risk taking (not perceived as risky), pushed some security prices to unsustainable levels, dramatically raised systemic leverage and thus, to use Minsky’s phrase, financial fragility (the vulnerability of the financial system to problems that appear anywhere within it), and facilitated the creation of unprecedented financial market complexity and opaqueness. They also led to a secular rise in the size of financial markets relative to the rest of the economy, and created the preconditions for a global financial crisis (Crotty, 2008). Once the crisis was underway, a liquidity trap ensued. Despite the federal funds rate being dropped nearly to zero, credit dried up in the interbank market requiring intervention from the Federal Reserve to facilitate loans and buyouts. Credit also dried up for the non-corporate business sector, which included smaller businesses despite banks sitting on large sums of cash and reserves unwilling to risk making bad loans (Pollin, 2012).

Businesses and financial firms were not the only ones who were overleveraged, households also became debt constrained. From 2000-2006, households experienced a sharp rise in debt primarily due to new borrowing (95 percent of which was comprised of mortgage debt), but also in part due to a rise in debt servicing from real interest rate growth outpacing real income growth (Mason and Jayadev, 2012). The severe devaluation in housing prices after the burst of the housing bubble resulted in households no longer able to borrow against their homes, and instead had to start repaying their mortgage debt (if possible). Although borrowing turned negative, there was little reduction in debt ratios for households as real income growth stagnated relative real interest rate growth (Mason and Jayadev, 2012). Between 2006 and 2008, household wealth plummeted by 25 percent ($17.6 trillion decrease), which according to research by Maki and Columbo (2001), assuming a modest wealth of effect of 3 percent, would reduce household spending by approximately $525 billion (Pollin, 2012). Such a massive reduction in spending due to a loss of wealth combined with a debt constrained household sector depressed consumer demand, and prolonged both the recession and the recovery after (Mason and Jayadev, 2012; Pollin, 2012; Eggertson and Krugman, 2012). There is also some empirical evidence suggesting the rise of income inequality since the 1970s are directly related to rising household debt. For example, Van Treeck and Sturn (2012) reference Pollin (1988) and Christen and Morgan (2005) empirical studies which identify a negative correlation between declining real median incomes and household debt and a positive correlation between increasing income inequality and household debt, respectively. The conclusion of these economists and others, essentially, is that consumers have used credit to compensate for their lack of income growth since the 1970s (see Rajan, 2010; Pollin 1988, 1990; Van Treeck and Sturn, 2012). While the trend in income inequality has persisted since the 1970s, the Great Recession has exacerbated the problem with the 1 percent receiving 93 percent of total income growth in 2010 according Saez (2012) (Pollin, 2012). And rising income inequality has only continued to get worse since then. Piketty, Saez, and Zucman (2016) report that “Income has boomed at the top: in 1980, top 1% adults earned on average 27 times more than bottom 50% adults, while they earn 81 times more today. The upsurge of top incomes was first a labor income phenomenon but has mostly been a capital income phenomenon since 2000. The government has offset only a small fraction of the increase in inequality.” While the financial sector and upper strata of income earners have recovered, the rest of the country is still struggling with anemic growth and continued stagnation in wage growth; ironically, as we debate more tax cuts for the rich. References Crotty, J. (2008). Structural Causes of the Global Financial Crisis: A Critical Assessment of the ‘New Financial Architecture’. University of Massachusetts - Amherst, Economics Department Working Paper Series No. 2008-14. Eggertson, G. B. and Krugman, P. (2012). Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo approach. The Quarterly Journal of Economics. 1469–1513. doi:10.1093/qje/qjs023 Mason J. W. and Jayadev, A. (2012). Fisher Dynamics in Household Debt: The Case of the United States, 1929-2011. Piketty,T., Saez, E. and Zucman, G. (2016). Distributional National Accounts: Methods and Estimates for the United States. The National Bureau of Economic Research. NBER Working Paper No. 22945. Pollin, R. (2012). The Great U.S. Liquidity Trap of 2009-11: Are We Stuck Pushing on Strings? Political Economy Research Institute. Working Paper Series No. 284. Van Treeck, T. and Sturn, S. (2012). Income inequality as a cause of the Great Recession? A survey of current debates. International Labour Office - Geneva: ILO, 2012. Conditions of Work and employment Series No. 39, ISSN 2226-8944 ; 2226-8952. J.M. Keynes’ policy proposals were much more radical than you were probably taught in university6/29/2018

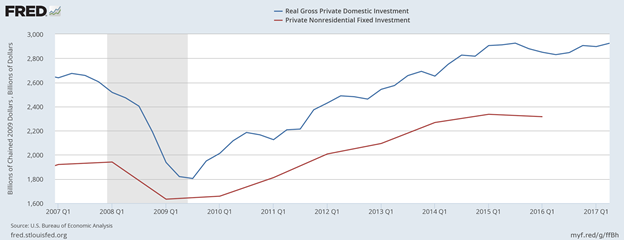

Contrary to what some economics textbooks might have you believe, John Maynard Keynes resoundingly rejected the classical paradigm, and, based on his policy prescriptions in The General Theory, he would have rejected the current mainstream macroeconomic policy tools of fiscal policy, taxation, and interest policy as the sole means of managing the business cycle. Rather, Keynes advocated for a much more interventionist role of government in public investment, “a somewhat comprehensive socialization of investment” as he referred to it, and a more long-term regime of low interest rate policy sufficient to push the economy to full employment. Keynes’ prognosis of the 1930’s economic malaise was due to the lack of effective aggregate demand which required sufficient investment to remedy. While public deficit spending could alleviate a downturn in the short-run, it would not be sufficient to prevent cyclical fluctuations in the long-run and keep the economy running at full-employment. As such, Keynes’ proposals could be considered quite radical relative to his time, and even current interventions used today. The current macro policy management kit consists of deficit spending and taxation (fiscal policy), and interest rates (monetary policy). Perhaps the best proxy for the mainstream (institutional) view on how these policy tools should be used is the current Federal Reserve Chair, Janet Yellen. Back in November, 2016, Yellen offered advice on fiscal policy just after the presidential election victory of Donald Trump. A major plank of Trump’s policy platform was infrastructure spending, but Yellen cautioned during congressional testimony to the Joint Economic Committee that “the economy is operating relatively close to full employment at this point,” so deficit spending would not have the same effect as it might have immediately after the Great Recession began in late 2007. She further cautioned that the new administration and Congress should be mindful of the debt: “With the debt-to-GDP ratio at around 77%, there’s not a lot of fiscal space should a shock to the economy occur, an adverse shock that did require fiscal stimulus.” Essentially, Yellen is suggesting that rather than wasting such an expenditure now, it would be better to save it until the next recession. On September 20th, 2017 Yellen gave remarks to the media regarding the Federal Open Market Committee’s decision to raise the federal funds rate from 1 percent to 1.25 percent, with a goal of 2.9 percent by 2020, as well as the announcement that the Fed will begin its “balance sheet normalization program” to reduce its nearly $4.5 trillion in securities holdings which resulted from its “quantitative easing” programs to reduce long-term interest rates. These decisions are indicative of the classical assumptions which have been embedded in New Keynesian macro theory, namely that the economy generally tends toward equilibrium, and these simple tools are sufficient for counter-cyclical management. As Yellen has testified, the mainstream establishment has the perception that the economy is doing better, and counter-cyclical tools are no longer necessary at this point. But, based on the proposals articulated in the The General Theory, Keynes would have disagreed. At the beginning of chapter 24 of his magnum opus, The General Theory of Employment Interest and Money, Keynes remarked that the two greatest flaws of modern capitalism were “its failure to provide full employment and its arbitrary and inequitable distribution of wealth and income.” The latter is made worse by the former, but both are viewed as non-issues in the classical paradigm. Progressive taxation has been one method by which to reduce inequality, but many worry about taking it too far; that it would reduce private investment and make the problem of unemployment and inequality that much worse. However, Keynes correctly identified that mass unemployment was caused by deficient aggregate demand, which in part was due to deficient investment. To address the issue of deficient investment, Keynes made two important proposals: 1) Low long-term interest rates equal to the marginal efficiency of capital. 2) The “socialization of investment.” The Fed’s quantitative easing (QE) program, which started under Chair Ben Bernanke, has been viewed as both innovative and extraordinary resulting in the long-term low interest rates since 2009. The purpose of this undertaking at the time was to provide a credible expectation to firms and entrepreneurs that rates of borrowing would be low for new capital investment. Despite QE, the shock of the downturn took a while to get over before private nonresidential investment began to pick up again in 2010 (see Fig. 1).  While one might be inclined to think that such a policy was original to Bernanke, in fact, Keynes advocated for central bank management of long-term interest rates through purchases of long-term securities in The General Theory (1936): [A] complex offer by the central bank to buy and sell at stated prices gilt-edged bonds of all maturities, in place of the single bank rate for short-term bills, is the most important practical improvement which can be made in the technique of monetary management…[However] The monetary authority often tends in practice concentrate upon short-term debts and to leave the price of long-term debts to be influenced by belated and imperfect reactions from the price of short-term debts; — though here again there is no reason why they need do so. The central bank can lower the short-term interest rates via purchases of short-term term securities in open-market operations, but this has no impact on long-term rates. Entrepreneurs and firms generally make long-term planning decisions based on what the government will do to short-term rates and may choose to hold off investment if they have reason to believe rates will not be favorable to them in the future. The central bank can address this by buying and selling long-term securities to provide a credible expectation that rates will be low in the long-term. This is indeed what the Fed did under Bernanke. But Keynes’ proposal was not that long-term rates should be kept low until the downturn was safely over and then raise them again. Instead, Keynes proposed low interest rates not only for the bust but also during the boom; even when the economy appeared to be “overheating” with wasteful investment and spending. [E]ven if over-investment in this sense [of being wasteful] was a normal characteristic of the boom, the remedy would not lie in clapping on a high rate of interest which would probably deter some useful investments and might further diminish the propensity to consume, but in taking drastic steps, by redistributing incomes or otherwise, to stimulate the propensity to consume… Thus the remedy for the boom is not a higher rate of interest but a lower rate of interest. For that may enable the so-called boom to last. The right remedy for the trade cycle [business cycle] is not to be found in abolishing booms and thus keeping us permanently in a semi-slump; but in abolishing slumps and thus keeping us permanently in a quasi-boom. The act of the monetary authority increasing interest rates has not only the effect of reducing investment, but also increasing unemployment, which in turn generates a further decrease in economic activity due to a decrease in demand. Thus, the current actions of the Fed to raise interest rates in a relatively meek growth environment, stagnant wages, and low labor force participation (relative to the pre-recession period) is exactly the opposite policy Keynes would have advocated. The level of aggregate demand depends on the level of employment and the propensity to consume, which is determined by the level of capital investment to create and expand firms to employ more people. However, due to the scarce nature of capital, sufficient investment alludes us and provides opportunity to the capitalist class to exploit that scarcity. “The owner of capital can obtain interest because capital is scarce, just as the owner of land can obtain rent because land is scarce. But whilst there may be intrinsic reasons for the scarcity of land, there are no intrinsic reasons for the scarcity of capital.” A means of reducing this scarcity, according to Keynes, is to “reduce the rate of interest to the level of the marginal efficiency of capital [net rate of return that is expected from the purchase of additional capital] at which there is full employment.” A low long-term interest environment can diminish the capacity to valorize capital in non-productive assets, pushing more investment into enterprise. [I]t would not be difficult to increase the stock of capital up to a point where its marginal efficiency had fallen to a very low figure. This would not mean that the use of capital instrument would cost almost nothing, but only that the return from them would have to cover little more than their exhaustion by wastage and obsolescence together with some margin to cover risk and the exercise of skill and judgement…Now, though this state of affairs would be quite compatible with some measure of individualism, yet it would mean the euthanasia of the rentier, and, consequently, the euthanasia of the cumulative oppressive power of the capitalist to exploit the scarcity-value of capital” (emphasis added). The “euthanasia of the rentier” would essentially be the castration of capitalist power over investment, and, therefore, over workers. However, interest rates alone are unlikely to be enough to ensure consistent investment up to the level of constant full employment, which brings us to Keynes’ other proposal. Looking at how “Keynesian” economics is practiced today, one would be inclined to think Keynes’ only contribution was to use government deficit spending on infrastructure, and, indeed, the U.S. infrastructure is in dire need of maintenance and would go a long way towards pushing the economy to full employment. However, Keynes wanted a more comprehensive intervention of the state in enterprise investment. “I conceive, therefore, that a somewhat comprehensive socialisation of investment will prove the only means of securing an approximation to full employment; though this need not exclude all manner of compromises and of devices by which public authority will co-operate with private initiative.” Keynes held these views for a long time. Prior to the publication of The General Theory, Keynes was active politically with the Liberal Party in Britain. According to James Crotty, in his book Capitalism, Macroeconomics and Reality: Understanding Globalization, Financialization, Competition and Crisis, Keynes was probably the “major force” in producing Britain’s Industrial Future (1928), a collective work of progressive proposals to improve Britain’s economy. Keynes proposed a new politically autonomous institution, like the Fed, called the Board of National Investment. Under the coordination of this “new and powerful” institution the state will be able to regulate the aggregate rate of growth of the economy by controlling the pace of public capital accumulation and directing investment toward the industries and areas hardest hit by structural unemployment. The Board was to control all the financial capital made available to public and semi-public concerns. It could borrow on its own account and was even authorized to lend to private companies. Keynes estimates that it would control 4 percent of GDP a year to start, and up to 8 percent of GDP in the foreseeable future.” This did not mean Keynes wanted a complete takeover of the economy by the state which he was careful to qualify in The General Theory: But beyond this no obvious case is made out for a system of State Socialism which would embrace most of the economic life of the community…[However] If the state is able to determine the aggregate amount of resources devoted to augmenting the instruments and the basic rate of reward to those who own them, it will have accomplished all that is necessary. Keynes clearly saw advantages in maintaining individual capitalism, mainly efficiency and personal freedom, and thought a comprehensive takeover of the state would sacrifice both as appeared to be the case in the Soviet Union in his time. But Keynes recognized that capitalism wasn’t perfect, it needed the strong guiding influence of the state to maintain full employment and temper the tempestuousness nature of the human economic activity which manifested so often in crises (e.g. The Financial Crisis).

If we define Keynesianism as the assumptions and tools used by macroeconomists today, then one may easily make the case even Keynes wasn’t a Keynesian. Keynes rejected erroneous assumptions about agents in the economy such as perfect competition, rational expectations, perfect foresight, and self-equilibrating markets. Simple manipulations of the interest rate and deficit spending have proven not enough to manage the economy and prevent crises. Keynes thought bigger and bolder with a larger role in mind for government to compensate for the inadequacies of capitalism; mainly as proposed in The General Theory, state control of investment and low long-term interest rates. The Fed was heading in the right direction by keeping interest rates low, but now it is regressing back again toward the status quo prior to the recession, raising interest rates at a time when wages are still stagnant and growth still relatively anemic. It is at the same time amazing and disturbing that mainstream introductory economics textbooks still teach fractional reserve banking and the money multiplier. Undergraduate students, myself included when I was an undergrad, learn that banks operate as intermediaries between savers and borrowers. For those with sufficient income to set some aside, you deposit that savings in a reputable bank. The bank in turn loans out those deposited funds to someone else at a profitable rate of interest. By loaning out your unused funds, this creates a multiplier effect by which the borrower spends the money which becomes someone else’s income, and so on. This assumption is crucial to monetarist theory. Banks are merely intermediaries between savers and borrowers; thus it is assumed that the money supply can be directly controlled using interest rate policy by the Federal Reserve. The only new money that can enter the system is through the government. A low interest rate policy by the Fed can increase demand for money loans, increasing the money supply, and reducing the rate would do the opposite. Government spending into the economy either by direct fiscal expenditure or injection of reserves into the banking sector would increase the money supply causing inflation from “too much money chasing too few goods” as Milton Friedman would say. Friedman argued that inflation could be stabilized by controlling the money supply through the interest rate; which exposed his ignorance to how money is actually created in the economy. Milton Friedman’s monetarism was based on the quantity theory of money which made two erroneous assumptions: (1) The growth rate of the money supply is the fundamental source of inflation, and (2) the supply of money is exogenous. For the first assumption to be true, the economy would need to be operating at full capacity and employment such that any increase in the money supply would increase demand beyond supply. For the second assumption to be true, banks would have to be constrained by the amount of deposits they have and the money supply could be controlled by manipulating the interest rate. As it turns out, banks do not need deposits to make loans. In reality, while money does take the form of deposits, banks are not limited by the amount of deposits they have in order to make a loan to a borrower whether a business or individual(s). This fact has been known for decades. The most prominent case is Joseph Schumpeter who wrote in 1954, “It is much more realistic to say that the banks ‘create credit,’ that is, that they create deposits in their act of lending, than to say that they lend the deposits that have been entrusted to them.” When banks make a loan they create two simultaneous entries on their balance sheet: one on the liability side in the form of a demand deposit for the borrower, and one on the asset side for the repayment of the loan by the borrower. Thus, loans create deposits, i.e. money, increasing the money supply. Many others that would follow Schumpeter such as Hyman Minsky, Nicholas Kaldor, Basil Moore, and others would further develop what has come to be known as the endogenous money view. But if the Federal Reserve is not the only source of money creation in the economy, then what tools does the Fed have to constrain the money supply? The Fed does control the reserve requirement ratio. The reserve requirement is the ratio of vault cash plus reserves relative to deposits the bank has on the liability side of its balance sheet. However, the required reserve ratio is seldom used. The current reserve ratio is 10 percent of deposits over 124.2 million. This means that when a bank creates a deposit, it does have to meet the requirement ratio by increasing the reserves in their Fed account by 10 percent of the amount of the loan deposit or cash on hand. Banks have several options to meet this requirement: (1) Banks can increase cash deposits or reserves by attracting new customers; (2) borrow money from other banks at the Federal Funds rate (or interbank rate); and or (3) borrow funds directly from the Fed at the discount window. Option (1) is the cheapest for them, so banks offer services and small interest benefits on deposits to attract customers. Option (3) is the most expensive for them. Alan Holmes, former vice chair of the New York Federal Reserve Bank, remarked, The idea of a regular injection of reserves-in some approaches at least-also suffers from a naive assumption that the banking system only expands loans after the System (or market factors) have put reserves in the banking system. In the real world, banks extend credit, creating deposits in the process, and look for the reserves later. The question then becomes one of whether and how the Federal Reserve will accommodate the demand for reserves. In the very short run, the Federal Reserve has little or no choice about accommodating that demand… (Homes, 1969; emphasis added). There is some dispute among proponents of endogenous money as to just how the Fed “accommodates that demand,” but most recognize that one way or another banks do find the reserves they need and focus very little on the reserve requirements. Bennett and Peristiani (2002) find that “reserve requirements have declined significantly in effectiveness, in the sense that they no longer appear to be as important a binding constraint on banks’ holdings of assets that qualify as reserves”. Thus, banks manage their reserves less to comply with regulatory minimums than to meet business needs and consumer demand, chasing reserves as they need them. The Fed also uses the Federal Funds rate. While the interest rate does influence demand for loanable funds, the fundamental determination of whether the bank will make the loan is the creditworthiness of the borrower and the general state of the economy. But the Fed does control, for the most part, over the Federal Funds rate which is the overnight interest rate at which banks loan to each other. The Federal Funds rate does influence the relative interest rate banks ultimately charge to make loans to consumers and businesses, and thus the growth rate of the money supply; however, it is not a direct control mechanism. Pollin (2008) finds some evidence of a causal relationship between the Federal Funds rate and market rates in the short-term, but no significant correlation in the long-term. Market forces, instead, appear to be “a major force-and are in most cases the major determinant-of market interest rates, especially at the long end of the markets”. Which means that to an extent, even market interest rates are endogenous to the financial system. Today, the Fed strives to target interest rates rather than monetary aggregates, but is not capable of “fine-tuning” as many believe. It is capable of “gross-tuning” meaning that changes in the Federal Funds rate can influence to some extent market interest rates. The Fed has proven it can exert moderate influence on long-term rates through its unconventional quantitative easing program by purchasing long-term bonds and assets, including mortgage backed securities guaranteed by the Federal government. But the more important function the Fed plays is the lender of last resort. The Fed proved how important this function was during the Great Financial Crisis of 2007–08. As commercial banks such as Bear Stearns, and some non-bank financial institutions such as AIG, found themselves in a liquidity crisis, the Fed stepped up, through intermediaries in some cases, with additional funds. Additionally, the Fed facilitated buyout arrangements which, while producing some moral hazard concerns, likely prevented a prolonged credit freeze which might have resulted in a more severe recession or a depression. I have used the term endogenous money to describe the process of above by which banks create money through loans. However, since this endogenous expansion of the money involves extending credit, endogenous finance might be just as appropriate; especially when speaking of more complex financial assets. Money serves three important functions: (1) a means of exchange; (2) a unit of account, and (3) a store of value. Any asset that exhibit these characteristics bears a degree of “moneyness.” More narrow measures include only the most liquid assets, the ones most easily used to spend in the economy such as currency, demand deposits, etc. Broader measures add less liquid types of assets such as certificates of deposit, savings deposits, small time deposits, and retail money market mutual funds; each of these being a financial innovation at one point in history. According to Pollin (2008), Innovation is a persistent feature of financial markets practices…Innovation in financial markets are primarily driven by efforts to enhance both the liquidity and store of value functions of any given financial asset, such as a Certificate of Deposit, a credit derivative, or securitized mortgage. Basically, this means lowering the costs of converting relatively high-yielding illiquid assets into liquid assets. To the degree that these financial innovations exhibit “moneyness,” measures of the money supply (e.g. M1, M2, M3, etc.) need to become more sophisticated and inclusive to better understand the impact on the economy. However, financial innovation bears two contradictory tendencies: (1) It relaxes the “saving-constraint,” and (2) it increases financial fragility. I will discuss both of these in turn. The mainstream view assumes that investment, and consumption for that matter, is constrained by savings. In this view, banks operate merely as intermediaries between savers and borrowers, investment and consumption cannot exceed the available amount of savings in the economy. The economy is “self-financed” and thus “savings-constrained.” Once one accepts the endogenous money view, it becomes immediately evident that savings becomes less of a constraint. Thus, banking institutions themselves are a financial innovation which relax this constraint since loans create deposits and increase the money supply. As more complex financial institutions and innovations introduce new forms of financial intermediation, the savings constraint becomes more and more relaxed. As put succinctly by Pollin (1997): Financial intermediation is the process whereby market participants, private institutions, and governments act to reduce information and transaction costs of financial provisioning, as well as allow for diversification of the risks associated with such activities. All else equal, reducing costs and diversifying risks through intermediation implies both that interest rates and collateral requirements on loans should fall in conjunction with declining costs of the diversification of risks. Financial innovation, in turn, is the process in which market participants create new channels and techniques of intermediation. In particular, asset and liability management techniques devised by intermediaries have created thick markets for liquidity. As we introduce more complex financial institutions (e.g. mutual funds, shadow banking system, etc.), government functions of financial intermediation (e.g. Federal Funds market, treasury securities, Bond sale and Repo market, etc.), and foreign financial intermediaries, information and transaction costs tend to come down, risk becomes more diversified, and more liquid assets are created weakening the “saving-constraint” through greater credit availability. The government especially plays a unique role here as it is the only institution that can create an exogenous injection funds into the economy. While every dollar produced is a liability on the government’s balance sheet, it bears no inherent default risk. To the extent that the government “finances” its injections as conventionally believed it needs to do, “it broadens its role as a financial intermediary,” and “creates further possibilities for the allocation of liquid assets” (Pollin, 1997). Government monetary institutional structures, regulatory regimes, and monetary policy shape the development of financial innovation; which also means that such innovation and structural complexity will vary across economies. Additionally, regulatory structures and general market conditions vary over time, and thus the innovation and structural changes in financial markets are also likely to vary over time. This means that the savings-constraint itself is likely to be variable over time. Pollin further points out, as any system grows in complexity, the innovative financial products and institutional structures tend to become permanent even when the conditions that produced them revert to normal states. This permanents builds on complexity in each era of innovation which contributes to financial fragility. This brings us to the negative tendency of financial innovation. The government has the unique role of regulating financial intermediation. Pollin (2008) notes, “the effects of [financial innovation] on market outcomes increase as the degree of market regulation declines.” As noted above, given permanent tendency of structural change, regulatory regimes are crucial to ensure a sound financial system. “Normal unregulated financial market practices inherently generate states of systemic instability, as financial market participants, operating to maximize profit under conditions of uncertainty, systemically assume riskier financial positions as cyclical expansions proceed”. The Neoliberal era has been marked by a dogmatic view of financial liberalization and deregulation. This was more or less the conventional wisdom in US leading up to the Financial Crisis of 2007–08. In his book, How Markets Fail, John Cassidy chronicles the deregulation of Wall Street for which Alan Greenspan was a central figure. “During the 1990s, he [Greenspan] played a key role in the dismantling of the Glass-Steagall Act, the Depression-era legislation that prevented depository institutions, such as Citigroup and Wells Fargo, from taking part in investment banking activities, such as peddling stocks, bonds, and mortgage securities”. Greenspan would go on to encourage the near full repeal of Glass-Steagall with the Gramm-Leach-Bliley Act of 1999. As derivatives came into prominence in the 1990s, “Greenspan, along with the Treasury, called on Congress to bar the CFTC [Commodity Futures Trading Commission] from regulating credit default swaps and other derivatives-a proposal that was passed into law the following year”. This is not to say that had all these prior regulations stayed in place that the financial system would not have been susceptible to systemic risk, but rollbacks in regulation opened the floodgates for rampant financial innovation and over leveraging in financial markets which undisputedly contributed to the Financial Crisis. References Bennett, Paul and Peristiani, Stavros (2002). “Are U.S. Reserve Requirements Still Binding?” Economic Policy Review, Volume 8, Number 1. Cassidy, John (2009). How Market Fail: The Logic of Economic Calamities. New York, NY: Picador. Holmes, Alan (1969). “Operational Constraints on the Stabilization of Money Supply Growth.” Controlling Monetary Aggregates. Conference Series №1. Federal Reserve Bank of Boston. Pollin, Robert (1997). The Macroeconomics of Saving, Finance, and Investment. Ann Arbor, MI: University of Michigan Press. Pollin, Robert (2008). “Considerations of Interest Rate Exogeneity.” Draft, August, 2008. Schumpeter, Joseph (1954). History of Economic Analysis. New York, NY: Oxford University Press |

AUTHORAaron Medlin is a PhD student at the University of Massachusetts Amherst studying macroeconomics of private debt, monetary economics, international finance, and comparative economic systems. Archives

July 2020

Categories

All

|

- CV

- Dissertation

- Job Market Paper

- Research

-

Teaching

- Intro Micro - mock syllabus

- Intermediate Macro - mock syllabus

- International Finance - mock syllabus

- Comparative Econ Systems - mock syllabus

- Applied Time Series - mock syllabus

- Econometrics - mock syllabus

- Econ 191 Economics Behind Our Lives (Fall 2021)

- Econ 204 Intermediate Macro (Summer 2021)

- Econ 397: Debt Economics (Spring 2021)

- Commentary

RSS Feed

RSS Feed