|

There are two key concepts we should keep in mind from Macro 101 as we think about both the circumstances of the COVID-19 crisis, and the government's response so far.

In response to the spread of the virus, Federal and state governments have recommended “social distancing” (more on this later), and some have declared a state of emergency to ensure it is enforced. This has resulted in the suspension of a great deal of everyday economic activity—that is spending on goods and services. This has led many restaurants, bars, and stores to shut down. It also means limited travel, especially overseas, which means very few people are flying. That is why the airline industry, for example, is hemorrhaging revenue and asking the government for a bailout. Again, spending is equal to income. That means the flow of income for businesses has stopped. Which means they cannot pay their workers. If workers in turn don’t have income, they cannot pay their rent or mortgage, their bills, or buy food. MONETARY POLICY RESPONSE: The disruption in the flow of income also makes for a disruption in the banking system which relies on a steady flow of your income to pass through them so they can make payments on your behalf and others, and pay their own obligations (e.g. interbank loans). Thus, the rapid and extraordinary response of the Fed to supply as much liquidity as needed to the banking system. Fed restarted QE (Quantitative Easing), which now allow banks to exchange multiple assets types—including treasuries, commercial bonds, mortgage backed securities, and even now municipal bonds—with the Fed for money. The Fed is making sure that markets for these securities don’t collapse, otherwise the prices of these assets would plummet because everyone is trying to sell them all at once, but no one is buying them. Therefore, the Fed has had to step in to be the buyer of last resort so to speak for these securities, which ensures their values do not fall to zero, and also provides the liquidity to the banking system and other economic participants who need it. The Fed has also dropped the policy interest rate to zero, or i = 0, to provide cheap credit to businesses in need. However, doing so in this case isn’t about spurring investment, it’s just to keep businesses a float long enough for the crisis to pass and economic activity to resume. FISCAL POLICY RESPONSE: To address the economic impact from social distancing measures, Congress has passed the CARES Act (or Coronavirus Aid, Relief, and Economic Security Act), a $2 trillion aid package to provide interim income for households and businesses to help them get through the crisis. According to NPR, the aid package is broken down as follows:

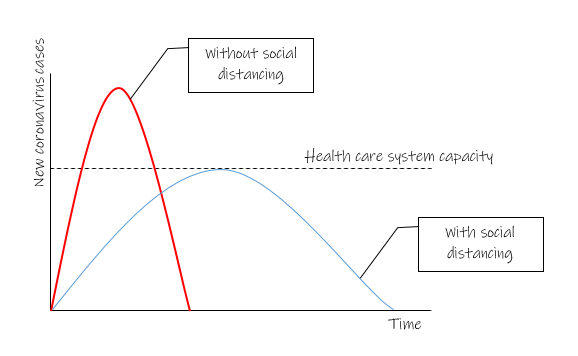

The point of the aid package is to restore some cash flows to households and businesses. The $339.8 billion to state and local governments is also very important. The Federal government prints our currency (in the US), and thus has unlimited finance to mobilize resources. State and local governments do not have this capacity, and instead rely on taxes and bonds issuances to raise revenue for public services. Since tax revenue is procyclical, meaning during a downturn revenue goes down (and up during a boom), local governments are experiencing a massive short fall in funding as well making it difficult to sustain essential public services. The last thing we want is for local governments to cut those essential services. State and local governments are also employ millions of people. So that aid package to states and local governments will help prevent cuts to services and more mass unemployment—something Federal government failed to do in during the Great Recession. And the Fed’s actions in accepting municipal bonds will also help prop up municipal bond markets. States are also the source of higher education funding. If states have to cut back on education funding for higher education, that means universities will need to raise tuition rates (which they had to do during the Great Recession), thus increasing the burden of student debt for future graduates. Unfortunately, the $2 trillion dollar aid package is not likely to be enough. It is also likely to be rolled out too slowly. There is a lot of bureaucracy is involved in getting the payments out, in applying for loans, and even for those who have already been laid off, applying for unemployment benefits. The longer it takes for people and businesses to receive aid, the deeper the recession will be. More aid will be needed. Just how much depends on how long this health crisis lasts. Then once the crisis is over, the government will need to think about an actual economic stimulus. When all is said and done, we are probably looking at several trillions of dollars needed to get the economy back on track to where were in terms of growth and employment before the crisis--which was just barely recovered to where we were before the Great Recession 10 years before that. You may have heard in the News that the purpose of social distancing is to “bend or flatten the curve.” What curve are they referring to exactly? And why is that important? Social distancing, or physical distancing, is maintaining a physical distance between you and other people and reducing the number of times you come into close contact with them in order to reduce the spread of a disease like COVID-19 or even the flu. The figure below illustrates why this is important so as not to overwhelm our health care resources. Notice the y-axis represents new cases of corona virus infections and the x-axis is time. The dotted line is the capacity of our health care system to handle demand. Uninhibited by social distancing measures, the red curve represents the trajectory of new cases that would occur as the virus spreads, which likely would overwhelm our health care capacity. Social distancing slows the spread so that our health care system can handle it. This is good, and it will save lives. But it also means we have to prolong the crisis as new cases will be stretched out longer over time. The longer it lasts, the deeper the economic impact will be without substantial aid from the government. Hope this is helpful. So remember to mind your distance. And pay attention to what the government is doing as it matters a lot for the outlook of the economy and the labor market once the immediate medical crisis is over.  Comments are closed.

|

AUTHORAaron Medlin is a PhD student at the University of Massachusetts Amherst studying macroeconomics of private debt, monetary economics, international finance, and comparative economic systems. Archives

July 2020

Categories

All

|

- CV

- Dissertation

- Job Market Paper

- Research

-

Teaching

- Intro Micro - mock syllabus

- Intermediate Macro - mock syllabus

- International Finance - mock syllabus

- Comparative Econ Systems - mock syllabus

- Applied Time Series - mock syllabus

- Econometrics - mock syllabus

- Econ 191 Economics Behind Our Lives (Fall 2021)

- Econ 204 Intermediate Macro (Summer 2021)

- Econ 397: Debt Economics (Spring 2021)

- Commentary

RSS Feed

RSS Feed