|

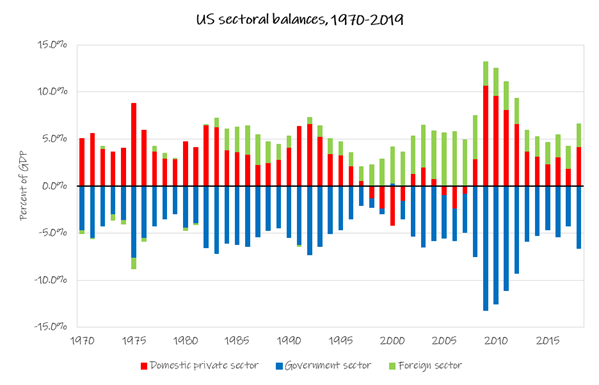

Stephanie Kelton’s new book, The Deficit Myth, is finally making the rounds of reviews by some economists and commentators. As is expected, there are some what-about-isms. In the case of Josh Mason's review in the American Prospect, the question is: what about banks? Now, The Deficit Myth isn’t meant to be "The Book" on Modern Monetary Theory (MMT). MMT as a body of work is a vast literature for which Kelton is attempting to condense a few very basic core arguments for a general non-academic audience. The confusion around public finance is hard enough to disentangle without bringing banks into the picture—which still required 300 plus pages. However, how bank money fits into MMT is one question, among others made in particular by Mason, worth addressing. Mason makes three main objections to Kelton’s arguments that I want to respond to. The first I have already mentioned above. Banks. Mason argues the existence of banks creates a "problem" for MMT's central claim that the government is the monopoly issuer of the currency. "Banks are money issuers every bit as much as the government. Government has tools to influence how much money is created by private banks, but its control isn't absolute. And when its control is effective, that's a function of the regulations and institutions of the financial system; it has nothing to do with the government monopoly on currency...Little is said about the private financial system." He also says that "Kelton, to be clear, never says anything factually untrue, but she gives the strong impression that the government is the only source of money that we use for transactions, which is not true at all." Second, Mason notes that while the federal debt is an important asset for the financial sector, it does not entirely correspond to the increase in private wealth. While you can make this claim tautologically, he argues, “it is false--asset values go up and down without any change in the government budget position.” Third, he argues the link between aggregate demand and supply is a historically contingent phenomenon and implies it is subject to change. And he expresses skepticism about the capacity of the Congressional Budget Office (CBO) to calculate the effect of spending on inflation any better than, say, the Federal Reserve can. Let’s tackle these arguments in order. The first thing to note is there is a difference between the currency proper, and other forms of private "money." (Money is too broad a term to be useful, but it basically implies it exhibits money functions, means of payment/exchange and store of value). The federal government is the only issuer of the currency proper. Full stop. It is illegal to counterfeit to Federal Reserve notes (bills) or coins. For electronic dollars generated by the Fed, i.e. reserves, it's the same. What banks, and other financial institutions, issue are various forms of financial instruments, contracts that differ in conditions of maturity (when the money has to be paid back), negotiability (transfer of ownership), and convertibility (to another asset). These instruments are debt contracts which promise to pay the government's currency. Bank deposits are a special sort of debt contract. Their maturity is zero. They are also negotiable, you can change the name on a checking account to someone else, or add someone to it. And most importantly, they are convertible on-demand to hard currency (bills and coins) or in reserves (electronic dollars) for settlement with another bank through the Federal Reserve System. To be clear, you as a customer cannot request that the bank give you Fed reserves. Customers may only have hard currency. Fed reserves would only be used when settlement between banks is required or when you pay your taxes to the government through your deposit account. Now, not all cases of settlement between deposits accounts have to be done through the Fed. For example, if two customers have deposits at the same bank, settlement occurs within the bank marking one account down and another up by the same amount. Some banks might also have deposit accounts with each other, and allow some limit of continuous overdraft credit, which at some point must be settled. This arrangement is called net clearing, or net settlement. Many larger banks are also members of the New York Clearing House which is a wholesale net clearing operation between banks, but one in which Fed reserves still play a role as any differences in credits and debits are turned over to the Federal Reserve Bank of New York for reserve settlement. Most transactions between banks, however, occur through Fed reserve settlement. What about bank loans? Don't loans create money? Yes, when banks make a loan, they create a deposit, which we noted exhibits the core functions of "money." In theory, there is no limit to the quantity of deposits a bank can create. You may have seen mailer ads, for example, from local banks offering some amount of money for setting up a checking account with them. I recently received one from Citizens Bank for a generous $400. Where does that money come from? The bank can simply create it as a deposit. But there is a practical limit to how much they are willing to create because deposits come with this condition of convertibility on demand to government money, which they do not create. This is where the Fed comes in. As banks expand deposit creation through loans, the Fed has to respond by creating adequate reserves so banks can service those deposits and ensure the payment system runs smoothly, so payments clear and checks don't bounce. This does not mean there needs to be a one-to-one relationship between the quantity of deposits and quantity of reserves, it simply means the banking system requires sufficient reserves circulating in the interbank lending market to ensure banks can maintain par value (i.e. parity) between bank money and government money. This institutional configuration is by design--a public-private partnership. The implication of this arrangement is that the Fed follows the lead of the private banking system to supply credit as needed to the public. Certainly, the private sector can get overzealous and create too much credit without adequate regulatory supervision. So while it is true that bank liabilities function as "money," as a store of value and means of payments/exchange, it is important to note that confidence in the use of that money is contingent on its convertibility on-demand from bank liabilities (bank deposits) to government liabilities (bills, coins, or reserves). If at any point a bank cannot convert your deposits to cash because, for example, a bank run, the bank fails; if it cannot obtain reserves to settle up with other banks, it fails. The former scenario was common before there was Federal deposit insurance. The latter was the main issue during the Great Financial Crisis--interbank lending came to a near halt and the Fed had to intervene as the lender of last resort. In heterodox economics, what I have just described above is called endogenous money theory, which flips the conventional wisdom that the Fed creates reserves, reserves create deposits, which banks then loan out to customers. Rather, bank loans create deposits, and the Fed responds by creating reserves. So endogenous money creation doesn’t break the link between deposits and reserves, it merely reverses the direction of causation from the conventional wisdom. Endogenous money theory is also a credit theory of money, which postulates that all money is an IOU, a debt, which anyone can create. “The trouble is getting it accepted” as the economist Hyman Minsky once said. But some proponents of this view lean too heavily on the "anyone can create money" insight, and forget or breeze through the rather hard part of "getting it accepted." In our modern financial system, most privately created financial instruments promise to pay government money or its practical equivalent which are bank deposits. This equivalence is accepted predominantly because of their convertibility to government money. And the government has set an expectation it will act as a backstop to this arrangement. So while banks can leverage government money in all sorts of ways that increase the "money" supply, the fact remains that banks are a user of government money just like any other non-government agent of the economy. The legal bank charter granted by the government which grants them special access to the Fed only reinforces this fact. Despite Mason’s argument, the existence of bank money has not been overlooked, nor does it undermine MMT’s claim about the sole currency issuer status of the government. Such statements, rather, suggest a certain level of ignorance of the endogenous money literature, let alone MMT. L. Randall Wray, for example, a founding MMT economist, and the first to author a book on the subject back in 1998, Understanding Modern Money: The Key to Full Employment and Price Stability, also happens to be one of the foremost scholars on endogenous money theory. He has written dozens of articles on the subject, and a book. I myself learned of endogenous money from Wray's 2012 primer on MMT, Modern Money Theory: A Primer On Macroeconomics For Sovereign Monetary Systems. So for as long as I have been studying MMT, I have also been studying endogenous money. If there is an inconsistency to be found, it isn’t there. ***** Some critics have argued that certain MMT conclusions rely on logical tautologies. To be clear, any statement that is deducible from a set of statements in some system of deduction within propositional logic, say a system of equations representing an economy, is in fact a tautology, i.e. true by construction of their logical form. Therefore, all conclusions derived from models in economics are tautologies. The question we should ask is whether the conclusions that result from those tautologies correspond to the real world. And if not, what is wrong with our initial premises from which those conclusions follow. Simply stating some conclusion is a tautology is not a valid argument against MMT or any theoretical model of the economy for that matter. You need to explain why the tautology in question is wrong. The claim Kelton is asserting, that the public sector deficit is equal to the private sector surplus, is derived from national accounting identities, which are the basis for how we construct our measure of GDP, which we aggregate from the summation of consumption, investment, government expenditure, and net exports. (1) GDP = C + I + G + (X - M) Equation (1) should be uncontroversial. This is how the Bureau of Economic Analysis calculates GDP. However, we can transform the equation to Gross National Product by brining in the net foreign income flows (FNI) which result from dividend and income flows of resident nationals abroad minus the flows to non-residents. (2) GNP = C + I + G + (X - M) + FNI The trade balance (X - M) plus FNI gives us the current account balance (CAB). (3) GNP = C + I + G + CAB We also generally define private sector savings as follows. (4) S = GNP - C - T Where T is taxes to the government. If we can agree on these definitions, then we should have no problem with the conclusion that follows when we derive the sectoral balances identity. Equation (5) follows from rearranging equation (4) such that GNP = S + C + T, moving C and T to the left hand side of the equation, and substituting it into equation (3). (5) S + C + T = C + I + G + CAB We can then rearrange the terms to the right side to get the sectoral balances equation in equation (4). (6) (S - I) + (T - G) + (-CAB) = 0 Fairly straight forward is not? In case it's not obvious though, (S - I) corresponds to the private sector balance (the different between expenditures and income), while (T - G) to the government sector balance. +CAB itself indicates the position of the domestic economy with respect to the rest of the world. Taking the negative of the current account (-CAB) tells the position of the rest of the world as a sector unto itself. Thus -CAB corresponds to the foreign sector balance. Assuming (CAB) = 0, for example, we could conclude from equation (6) that S > I (private sector surplus) is only achievable when T < G (public sector deficit) to maintain equality to zero. We can also confirm this using real-world data. The figure below plots the net lending/borrowing for the private sector (household, firms, etc.) and the government sector, with the foreign sector represented by the negative of the US current account position. The data is constructed from the National Income and Product Accounts (NIPAs) compiled by the Bureau of Economic Analysis (BEA). We can interpret bars above zero as being in surplus, while bars below zero means the sector is in deficit. This is why we take the negative of the current account position, to reflect that the foreign sector has a trade surplus when we (the US) are in deficit. Notice the bars mirror each other; indicating if the values of each sector's balance were added together, they would equal zero, just like our identity in equation (6).  So we have proven Kelton’s claim mathematically using conventional accounting identities, and we have verified it with data. Therefore, to properly debunk it, you have to go back to our initial definitions and explain what is missing. Now we can also rearrange equation (6) in another way that makes it more explicit that private savings are a function of private sector borrowing and government expenditure. (7) S = I + (G - T) + (CAB) Equation (7) confirms private sector savings is a function of investment, which is financed these days mostly out of savings by firms but also bank credit and debt securities, as well as the government's deficit position, and the current account balance. This also captures both what Kelton is describing, government deficits equal private savings, but also Mason's point about money creation by banks to firms for investment which also creates private savings. However, net financial wealth for the private sector is still defined as (S - I), which means assets and liabilities net to zero in the aggregate for the sector as a whole--unless an external sector, either the government sector and or the foreign sector, is running a deficit. ***** Mason's comment regarding the fluctuations in value of private assets is a bit of a red herring and a good example of the fallacy of composition. All else constant, fluctuations in asset values occur through the buying and selling of those assets. If the price of a given asset increases, that is because there is now more demand for that asset than there were willing suppliers. The exchange of money for that asset just shifts around money values between traders. Mason is guilty of the fallacy of composition here because although an asset, or class of assets, maybe appreciating in value, it does not mean that net private sector wealth is also increasing in the aggregate. It just means that wealth has shifted from one group to another within the sector. Mason's observation that the correlation between expenditure and inflation is historically contingent is an important one, but that contingency is not a mystery. It is because the US has strong political and monetary institutions. None of this is lost on MMTers who account for this in their framework using the concept of "monetary sovereignty." A government with a high degree of monetary sovereignty generally has to meet five criteria. (1) The national government chooses the unit of account and issues currency denominated in that unit; (2) imposes a debt obligation in that unit, and (3) accepts its own currency in payment of that obligation; (4) only denominates debt instruments against itself in that unit; and (5) floats its exchange rate (if it's going to operate with an open capital account). A country with less than reliable political and monetary institutions will be subject to economic volatility as confidence in those institutions wanes. No one, especially MMT scholars, is suggesting achieving these criteria is easy. I suspect countries bountiful in natural resources, particularly in food and energy, with a highly educated workforce, and robust political institutions, will have an easier time of it than others. Although the club of monetary sovereigns is relatively small, they have significant sway over the rest of the world economy. MMT provides a lens by which to study them and understand their advantages. There is no reason in principle why many countries could not have the level of monetary sovereignty Canada, Australia, or Japan have achieved. This is also not to disregard the political economy of the international monetary system (IMS). Indeed, there are power dynamics between countries, particularly the global north and global south which make the task of achieving monetary sovereignty even more difficult, if not impossible in some cases without reform of the IMS. This is also not lost on MMT scholars, and one could argue that this aspect of MMT has not been theorized enough. But even lacking substantive reform to the IMS, there are steps developing and emerging market countries can take to attain a greater degree of monetary sovereignty, but it requires dispelling myths and doing away with the conventional framework of mainstream economics which paralyzes countries from the start. ***** Lastly, whether the Congressional Budget Office (CBO) would be the best institution to determine the impact of government spending on inflation in the economy is not really the point Kelton is making. Certainly, MMTers would not argue the CBO as presently constituted has this capacity. Nor does the Fed. The Fed’s own theory of inflation, which relies on the flawed non-accelerating interest rate of unemployment (NAIRU) paradigm, is in crisis. One Fed official admitted as much in 2017. The Financial Times reported Daniel Turillo, who had recently retired from the Fed's board of governors that year, said in a speech that economists display "a paradoxical faith in the usefulness of unobservable concepts such as the natural rate of unemployment or neutral real rate of interest, even as they expressed doubts about how robust those concepts were." Quoting him directly, Turillo was unequivocal about the problem facing policymakers at the Fed, "we do not, at present, have a theory of inflation dynamics that works sufficiently well to be of use for the business of real-time monetary policymaking." What Kelton is arguing for is the establishment of new institutional capacity, one staffed with experts capable of appropriately assessing the nation's real supply constraints. The US used to have this institutional capacity--as Kelton has noted in prior interviews. During World War II, the National Resources Planning Board (1933 - 1943) was responsible for managing an inventory of the nation’s resources and inflation pressures during the war. Its “advisory [role in] national planning became a policy process bringing together social scientists, executive and legislative branches, and private and public institutions.” It was staffed with “experts, temporary consultants, and field branches [which] conducted studies of land use, multi-use water planning, natural resources, population, industrial structure, transportation, science, and technology that provided the first national inventories of significant American resources.” However, NRPB was relatively short-lived, and chronically underfunded. But whether it’s a reconstituted NRPB, a reformed CBO, or even the Fed is not Kelton’s point. The point is this isn’t remotely how we assess public spending currently. Conclusion Mason obviously isn't the first to bring up some of these arguments. I'm only picking on him because he is a fellow heterodox economist, and I respect him. But it is frustrating that these same what-about-isms come up again and again without effort to address the already vast literature that has confronted these issues. There are two key concepts we should keep in mind from Macro 101 as we think about both the circumstances of the COVID-19 crisis, and the government's response so far.

In response to the spread of the virus, Federal and state governments have recommended “social distancing” (more on this later), and some have declared a state of emergency to ensure it is enforced. This has resulted in the suspension of a great deal of everyday economic activity—that is spending on goods and services. This has led many restaurants, bars, and stores to shut down. It also means limited travel, especially overseas, which means very few people are flying. That is why the airline industry, for example, is hemorrhaging revenue and asking the government for a bailout. Again, spending is equal to income. That means the flow of income for businesses has stopped. Which means they cannot pay their workers. If workers in turn don’t have income, they cannot pay their rent or mortgage, their bills, or buy food. MONETARY POLICY RESPONSE: The disruption in the flow of income also makes for a disruption in the banking system which relies on a steady flow of your income to pass through them so they can make payments on your behalf and others, and pay their own obligations (e.g. interbank loans). Thus, the rapid and extraordinary response of the Fed to supply as much liquidity as needed to the banking system. Fed restarted QE (Quantitative Easing), which now allow banks to exchange multiple assets types—including treasuries, commercial bonds, mortgage backed securities, and even now municipal bonds—with the Fed for money. The Fed is making sure that markets for these securities don’t collapse, otherwise the prices of these assets would plummet because everyone is trying to sell them all at once, but no one is buying them. Therefore, the Fed has had to step in to be the buyer of last resort so to speak for these securities, which ensures their values do not fall to zero, and also provides the liquidity to the banking system and other economic participants who need it. The Fed has also dropped the policy interest rate to zero, or i = 0, to provide cheap credit to businesses in need. However, doing so in this case isn’t about spurring investment, it’s just to keep businesses a float long enough for the crisis to pass and economic activity to resume. FISCAL POLICY RESPONSE: To address the economic impact from social distancing measures, Congress has passed the CARES Act (or Coronavirus Aid, Relief, and Economic Security Act), a $2 trillion aid package to provide interim income for households and businesses to help them get through the crisis. According to NPR, the aid package is broken down as follows:

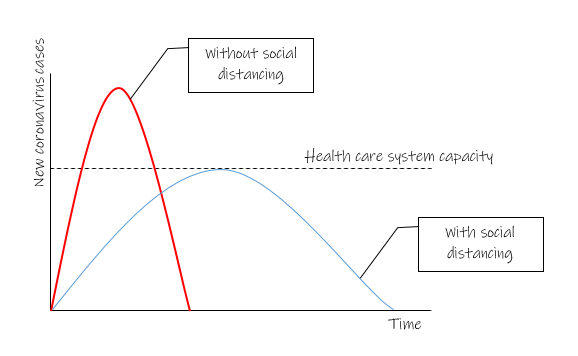

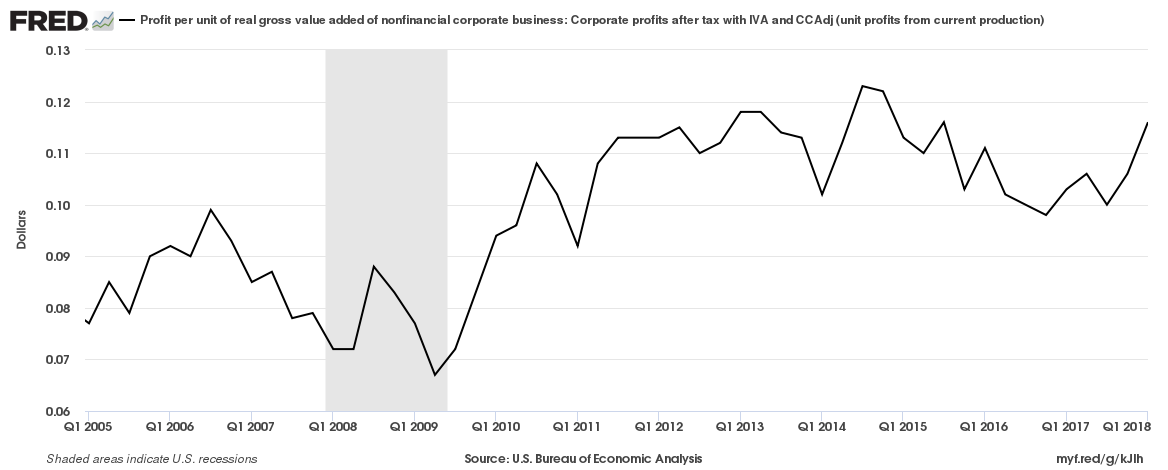

The point of the aid package is to restore some cash flows to households and businesses. The $339.8 billion to state and local governments is also very important. The Federal government prints our currency (in the US), and thus has unlimited finance to mobilize resources. State and local governments do not have this capacity, and instead rely on taxes and bonds issuances to raise revenue for public services. Since tax revenue is procyclical, meaning during a downturn revenue goes down (and up during a boom), local governments are experiencing a massive short fall in funding as well making it difficult to sustain essential public services. The last thing we want is for local governments to cut those essential services. State and local governments are also employ millions of people. So that aid package to states and local governments will help prevent cuts to services and more mass unemployment—something Federal government failed to do in during the Great Recession. And the Fed’s actions in accepting municipal bonds will also help prop up municipal bond markets. States are also the source of higher education funding. If states have to cut back on education funding for higher education, that means universities will need to raise tuition rates (which they had to do during the Great Recession), thus increasing the burden of student debt for future graduates. Unfortunately, the $2 trillion dollar aid package is not likely to be enough. It is also likely to be rolled out too slowly. There is a lot of bureaucracy is involved in getting the payments out, in applying for loans, and even for those who have already been laid off, applying for unemployment benefits. The longer it takes for people and businesses to receive aid, the deeper the recession will be. More aid will be needed. Just how much depends on how long this health crisis lasts. Then once the crisis is over, the government will need to think about an actual economic stimulus. When all is said and done, we are probably looking at several trillions of dollars needed to get the economy back on track to where were in terms of growth and employment before the crisis--which was just barely recovered to where we were before the Great Recession 10 years before that. You may have heard in the News that the purpose of social distancing is to “bend or flatten the curve.” What curve are they referring to exactly? And why is that important? Social distancing, or physical distancing, is maintaining a physical distance between you and other people and reducing the number of times you come into close contact with them in order to reduce the spread of a disease like COVID-19 or even the flu. The figure below illustrates why this is important so as not to overwhelm our health care resources. Notice the y-axis represents new cases of corona virus infections and the x-axis is time. The dotted line is the capacity of our health care system to handle demand. Uninhibited by social distancing measures, the red curve represents the trajectory of new cases that would occur as the virus spreads, which likely would overwhelm our health care capacity. Social distancing slows the spread so that our health care system can handle it. This is good, and it will save lives. But it also means we have to prolong the crisis as new cases will be stretched out longer over time. The longer it lasts, the deeper the economic impact will be without substantial aid from the government. Hope this is helpful. So remember to mind your distance. And pay attention to what the government is doing as it matters a lot for the outlook of the economy and the labor market once the immediate medical crisis is over.  Nominal wages are not the whole story. The media likes to report nominal figures which can give news consumers a false sense of the trends. But in a monetary economy with inflation (increasing prices), nominal figures tell you almost nothing. Using real numbers, which are adjusted for inflation, give you a much better sense of what is really going on in terms of actual gains and purchasing power for workers. For example, if your salary has increased 2-percent, but the cost of everything has also increased 2-percent, you are not earning more than you did before in real terms. So when you see news media reporting nominal figures, you should be skeptical of any reported trend, and what it means for the economy, until you see the REAL figures. Exhibit A: Bloomberg recently reported that compensation benefits are going up. Reporting on the Employment Cost Index (ECI) from the Bureau of Labor Statistics (BLS), their key takeaway was that these “latest results [from the report] indicate employers are offering better compensation packages to workers amid an ongoing shortage of qualified workers”, and more or less leave it at that. Exhibit B: The Wall Street Journal, reporting from the same ECI release, declared “ U.S. workers received their biggest pay increases in nearly a decade over the 12 months through June, a sign the strong labor market is boosting wages as employers compete for scarcer workers.” Other media outlets that have picked up on the good news have shown a little more skepticism, but little effort to find out the REAL story. The problem is that this is not exactly what the ECI report said in the first place, and it doesn’t account for inflation. The first thing you should know about the Employment Cost Index is that it reports total employment compensation costs in nominal terms across the economy. It also breaks it down into private and public sectors. Looking at private sector employment costs, the report does indicate that compensation costs have risen 2.9-percent year-over-year (i.e. in the past 12 months). This includes both wages and salaries (which account for 70-percent of compensation costs) and benefits (which make up the other 30-percent). Let’s focus on wages and salaries first. According to the ECI report, wages and salaries increased in the last 12 months 2.9-percent in nominal terms. Conveniently, the BLS also releases a report on REAL wage earnings. According to the most recent release, from May to June 2018, real average earnings increased only 0.1-percent. That’s one-tenth of a percent people, that’s nothing! And when the BLS looked back further, it found there has been no change at all in the past year: “From June 2017 to June 2018, real average hourly earnings decreased 0.2 percent, seasonally adjusted. Combining the change in real average hourly earnings with a 0.3-percent increase in the average workweek resulted in no change to real average weekly earnings over this period.” Let’s breakdown what that means. Private sector workers are earning less than they were 12 months ago, and are working more hours to makeup for it to maintain the same level income. That is a much bleaker picture than what the nominal figures suggest. What about the benefits in these “better” compensation packages. It should also be noted that ECI includes healthcare insurance benefits. The report does indicate overall benefit costs have increased by 2.9-percent between June 2017 and June 2018, but it also indicates 1.9-percent of that increase was due to increasing health insurance costs. So that leaves 0.3-percent increase in the last 12 months for monetary benefits other than healthcare insurance. But this is still a nominal figure. After you account for inflation, it evaporates. The most recent release of figures for inflation by the BLS as measured by the Consumer Price Index shows an increase of 2.9-percent for the same period before seasonal adjustment. But even after adjustment, what are the chances it gets revised down more than 2.6-percent to break-even on those “greater” benefits workers supposedly are getting? Quite low you can be sure. Which means that when it comes to REAL gains in benefits, workers are actually in the red while real earnings have not moved.  Who gains from this particularly rosy picture of the economy is unclear. It certainly makes the Trump Administration look good. Some media outlets perhaps are just looking for a positive story given our democracy may be on the verge of implosion. Who knows. But these supposedly economic literate media outlets are not doing you any favors by reporting nominal figures that misrepresent what workers in the economy are actually experiencing in terms of real purchasing power even as real profits continue to increase for businesses (see Figure above). This little extra piece of context makes the story even more bleak. Businesses are earning more in real terms than they were before the recession, but not sharing the gains with workers whose purchasing power is eroding to the extent that they need to work more hours to maintain their standard of living. That is the real story behind these ECI numbers, but that would contradict the “strong labor market” narrative.

Given the recent Supreme Court decision in Janus v. AFSCME, the public sector union case, I thought it worth explaining why labor unions are so important aside from the usual explanations given.

In 1956, Richard Lipsey and Kelvin Lancaster, developed the Theory of Second Best for the Walrasian model. They demonstrated in their paper that when one optimality condition cannot be satisfied, manipulating other variables away from optimum can create a second best outcome in an economic model. In other words, if one market distortion cannot be removed, then a second best equilibrium can be achieved by imposing a second market distortion. The Theory of Second Best can explain why labor unions are not distortionary, but counter distortionary to the general state of the labor market. If you have taken an introductory economics course, you might be vaguely familiar with the argument that unions create a distortion to the economy. By unions demanding higher compensation above the equilibrium wage, the union creates a surplus of labor since labor demand at the higher wage is lower than the equilibrium wage. The problem with this argument is it assumes a perfectly competitive labor market. The reality is that in most labor markets have significant imperfections. Labor market frictions are pervasive. Regional monopolies are pervasive creating monopsony markets for certain labor skills (if you are unfamiliar with the concept of monopsony, I have written about it before here). Even while certain regions encompass enclaves of industry, differentiation between firms can produce inadequate alternatives based on individual preferences. Commuting distances and tenure benefits create disincentives to move between jobs. Imperfect information between firms and workers is also a crucial assumption of the perfectly competitive market, yet we know perfect information is not possible, nor even desirable to both parties. All of these market imperfections give firms a non-negligible influence over wages; evidenced by the fact that real wage earnings have been stagnant since the 1970s. The natural state of the labor market is a distorted state which carries with a less than social optimal equilibrium. The market imperfections are not easily corrected or removed. Technology may reduce search frictions by increasing the probability of matches through online job search sites, but fixing geographical distances, compensating differentials, and reducing the monopolies requires structural adjustment to the economy that come at no small cost. This is why unions are so important. They were created in response to these imperfections which gave firms undue influence over wages. Unions become a countervailing force to the monopsony power of firms. The decision in Janus of course has dealt a significant blow to financing of public sector unions. For those that don’t know—which is understandable given our crazy news cycle these days—this Supreme Court overturned 41 year old precedent set in Abood v. Detroit Board of Education (1977) which permitted unions to charge an “agency fee”. Agency fee was a compromise the court made for non-union employees who may have disapproved or did not want to contribute to the political activities of unions, but nonetheless enjoyed the compensation gains earned from union bargaining activity. Since non-union employees were only paying for bargaining activity, agency fees were less than actual union dues. The arrangement seems to have worked pretty well for over 40 years until Janus, which ruled that agency fees were unconstitutional. This puts unions, whose influence and power have already been diminished considerable over the last couple decades, between a rock and a hard place. The law of the land is that unions still have to represent all employees of a company, state, or municipal government. However, it can no longer charge the agency fee, which will create free riders, and unions will now have to divert funds into union member recruitment and retention. There is no question it’s a significant blow in the short-term, but there is an argument to be made that it could make unions stronger in time. Only time will tell. And it’s imperative that they do because unions are crucial the balance of power between monopolies and labor, and the theory of second best explains why. Vox Media has an interesting YouTube video floating around on Facebook about pennies (see below). If you haven’t seen it, you have probably heard a take on the theme: pennies are useless and cost the government more money to make them than they are worth ($0.0107 per penny). While this is true, one might be misled into believing that the government is somehow losing millions of dollars from the manufacturing of the currency, but it’s not when you factor in the rest of coins and bills the U.S. produces into the equation. In monetary economics, there is a concept called “seigniorage”; which dates back to the Middle Ages from Old French seigneuriage “right of the lord (seigneur) to mint money”. Seigniorage is generally defined as the net revenue or profit, if you will, from the face value of the coinage or token minted minus the cost of production and maintenance. For example, the cost of producing a dollar bill is a couple cents (say $0.05), so the rest of the value generated by producing a dollar bill ($0.95) counts as revenue to the treasury. So even though it costs $0.0107 to make a penny, the treasury is not losing money when you factor in the combined seigniorage revenue from all the coins and bills produced into circulation; it’s still a huge positive net revenue. In 2016, in fact, the U.S. Mint reported seigniorage net income of $668.5 million before protection costs.

So while it’s true that pennies cost, and maybe they are useless, it’s not really a big deal to keep them either. By getting rid of them, it would simply increase the net revenue to the treasury. Personally, I would be fine with getting rid of them, and it would not be an issue as many countries have already done it such as Canada and Australia. But let’s not overreact to the cost of producing them when you consider how much seigniorage revenue is still gained from producing $5, $10 bills, $20 bills, etc. |

AUTHORAaron Medlin is a PhD student at the University of Massachusetts Amherst studying macroeconomics of private debt, monetary economics, international finance, and comparative economic systems. Archives

July 2020

Categories

All

|

- CV

- Dissertation

- Job Market Paper

- Research

-

Teaching

- Intro Micro - mock syllabus

- Intermediate Macro - mock syllabus

- International Finance - mock syllabus

- Comparative Econ Systems - mock syllabus

- Applied Time Series - mock syllabus

- Econometrics - mock syllabus

- Econ 191 Economics Behind Our Lives (Fall 2021)

- Econ 204 Intermediate Macro (Summer 2021)

- Econ 397: Debt Economics (Spring 2021)

- Commentary

RSS Feed

RSS Feed